This story is part of an NPR series, We Hold These Truths, on American democracy.

Last summer, DonnaLee Norrington had a dream about owning a home. Not the figurative kind, but a literal dream, as she slept in the rental studio apartment in South Los Angeles that she was sharing with a friend.

At around 2 a.m., Norrington remembers, “God said to me, ‘Why don’t you get a mortgage that doesn’t move?’ And in my head I knew that meant a fixed mortgage.”

The very next morning — she made an appointment with Mark Alston, a local mortgage broker well known in the South LA Black community, to inquire about purchasing her very own home for the first time.

She was 59 at the time.

Alston has built his lending practice on the hope of expanding access to homeownership for Black Americans. He says they have been systematically discriminated against by the real estate industry and government policy. Unlike most loan officers, Alston works with his clients for months — even years — to disentangle a convoluted loan application process, pay off bills and boost credit scores so they can ultimately qualify for a home loan.

Today, Norrington and her younger sister MaryJosephine Norrington own a three-bedroom house in Compton, where three generations of her family currently live.

Owning a home is an undeniable part of the American dream — and of American citizenship. It is also the key to building intergenerational wealth. But Norrington’s homeownership success story is an increasingly rare one for Black Americans.

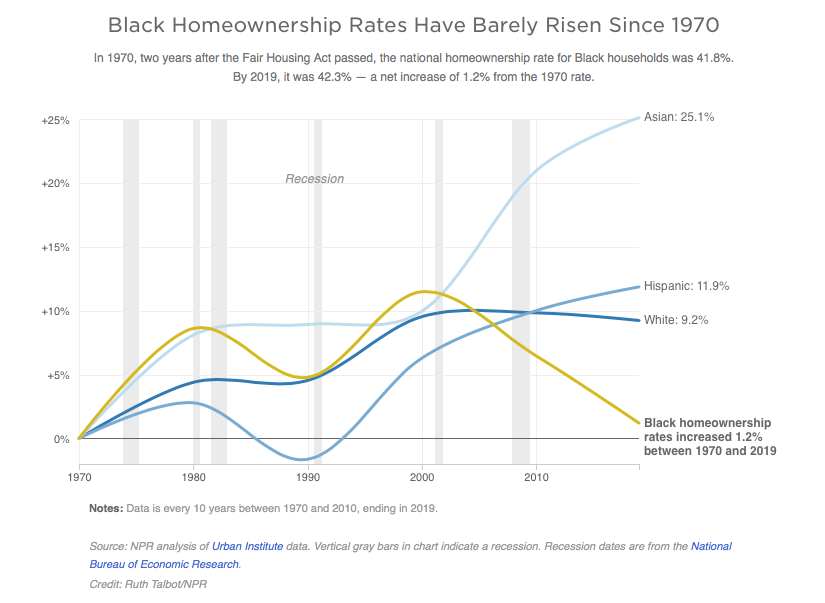

Over the last 15 years, Black homeownership has declined more dramatically than for any other racial or ethnic group in the United States. In 2019, the Black homeownership rate was about as low as in the 1960s, when private race-based discrimination was legal.

The story of housing discrimination is rooted in a long history of racist government policies perpetuated by the real estate industry and private attitudes that began with slavery. The federal government began to push and expand homeownership in the New Deal era through innovations like the 30-year mortgage.

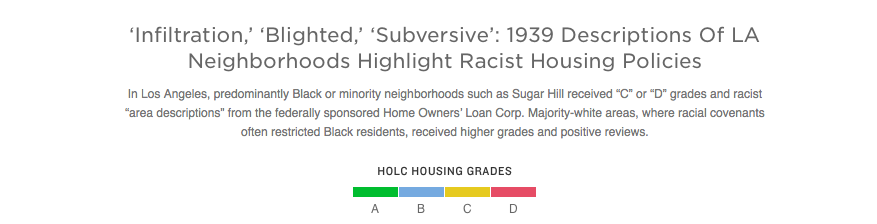

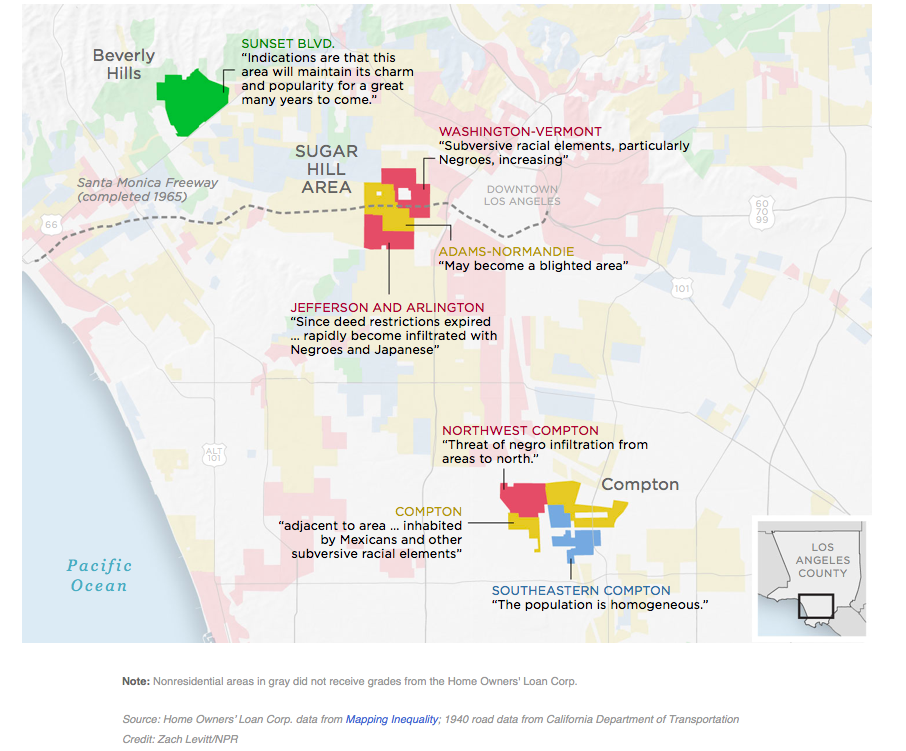

But one way Black people and other minority groups were left out systematically was through a process known as “redlining” which labeled certain areas as “risky” for a home loan. African Americans and immigrants were relegated to areas, marked in red on government-sponsored maps, where poverty was most concentrated and housing was deteriorating.

The Fair Housing Act of 1968 recognized segregationist practices like redlining to be unconstitutional. But the law only prohibited future, formalized discrimination rather than undoing the foundationally racist landscape on which homeownership in America was built.

The vicious cycle and legacy of redlining has persisted: Residents of redlined communities struggled to receive loans to buy or renovate their homes, which led to disrepair and a decline of a community’s housing stock. That in turn forced businesses to close and depressed tax revenue, diminishing school funding.

Today, many of the same neighborhoods that were redlined continue not only to have the highest poverty rates, but also worse health outcomes that lead to shorter lifespans. And Black Americans are nearly five times more likely to own a home in a formerly redlined neighborhood than in a greenlined, or “desirable,” neighborhood, resulting in less home equity than white Americans have.

The West Coast has often held hope as a cultural and political promised land for marginalized groups. During the first and second Great Migrations, millions of Black Americans moved west to escape the Jim Crow South in search of more equal treatment and opportunities — in part, because legal, racist policies and practices were so widespread all across the country at that time.

But while Los Angeles, one of California’s major metropolises, would become the battleground for hard-fought civil rights victories for Black Americans, it was also a place where housing segregation, predatory real estate practices and exploitative lending thrived.

Our story begins with one Los Angeles neighborhood, known as Sugar Hill, where the Black community successfully fought racially restrictive covenants only to later face another threat — from the freeway.

The tree-lined boulevards of the West Adams neighborhood are studded with stately homes.

“That was Marvin Gaye’s place right there,” says Rha Nickerson, who grew up in the area, as she points to one such two-story house on Gramercy Place.

It’s easy to tell from the ornate architecture of the houses, the antique street lights and the wide roads that the neighborhood bore witness to a lot of history. But it’s hard to miss the loud hum of the Santa Monica I-10 freeway coming from behind a large concrete wall at the end of Marvin Gaye’s street.

Siblings Rha and Van Nickerson are now 73 and 72, respectively. They spent formative years of their childhoods in this neighborhood, which was once called Sugar Hill — a nod to the thriving Black Harlem Renaissance neighborhood of the same name. Doctors, entrepreneurs and oil barons lived in Sugar Hill — even legendary stars like jazz singer Ethel Waters and Gone with the Wind actress Hattie McDaniel.

But Sugar Hill’s thriving Black community was an exception: It managed to exist despite systemic efforts to prevent Black people from buying homes in much of Los Angeles.

One of the most prevalent tools white residents used to maintain the segregation — across America and in Sugar Hill — was the racially restrictive covenant. These agreements, embedded in property deeds, made homeowners promise never to sell to African Americans or other minority groups. In 1940, 80% of properties in Los Angeles had these restrictions attached to them.

Rha Nickerson remembers her father teaching her about these covenants when she was a young girl, and says that it was only because people like Hattie McDaniel fought these restrictions that her family was able to live there.

Racially restrictive covenants were ubiquitous in Sugar Hill at the time, like many places in America. But some white homeowners willingly violated them to sell to Black buyers, in part because Black people were willing to pay more since there was far less property available to them. The willingness to violate covenants was especially the case around the Great Depression, when many homeowners were desperate to sell.

The first African American known to purchase a home in Sugar Hill was entrepreneur Norman Houston, who bought property in 1938. In the years following, a wave of Black families moved into the area.

But one white homeowners association did not like the way its neighborhood was changing. So members of the West Adams Heights Improvement Association sued their Black neighbors for violating racially restrictive covenants in hopes of having them evicted — even though white sellers had violated the covenants.

McDaniel, Houston and their neighbors fought back with their own Black homeowners association called the West Adams Heights Protective Association. Two of Houston’s grandchildren, Ivan Houston and Kathi Houston-Berryman, say they remember their grandfather as a leader in the movement for housing justice for Black Angelenos.

“He always did have a vision and I think he was what is known as a pacesetter … because he was always moving ahead,” Houston-Berryman says. Ivan still has his grandfather’s notebook that documented the West Adams Heights Protective Association meeting minutes, including the discussions the group had about fighting racially restrictive covenants.

After years of planning, the parties involved with what came to be known as the “Sugar Hill case” took to the Los Angeles Superior Court on the morning of Dec. 5, 1945. Hattie McDaniel, her codefendants, and 250 sympathizers “appeared in all their finery and elegance.”

The white plaintiffs claimed Black homeowners in Sugar Hill would lead to declining property values in the neighborhood, even though their Black neighbors had well-maintained properties with increasing home values. Such racist thinking was in line with the dominant logic of the real estate industry at the time — the logic underlying redlining.

In his retort, civil rights attorney Loren Miller, who represented the Black homeowners, used an argument that had never worked in any U.S. court before — that restrictive covenants violated the California Constitution and the 14th Amendment, which mandates equal protection under the law.

Taking the packed courtroom by surprise, Judge Thurmond Clarke ruled in favor of Miller. “Certainly there was no discrimination against the Negro race when it came to calling upon its members to die on the battlefields in defense of this country in the war just ended,” Clarke said.

This victory did not just mean the Black residents of Sugar Hill got to stay in their homes — it set a precedent for the 1948 U.S. Supreme Court Case Shelley v. Kraemer, also argued by Miller, that would deem racially restrictive covenants unenforceable.

Amina Hassan, who has written a biography about Miller, says the win was monumental because “housing was the crux of it all.” She says access to safe, quality housing meant Black people could “have their children in better schools, they could find jobs in the area. Housing was the key to greater wealth.”

In 1952, a few years after the Supreme Court ruling, Rha and Van Nickerson’s family moved into the Berkeley Square community of Sugar Hill. The siblings’ eyes light up recounting their childhood there.

“We got our wagon and we’d go up and down the street and selling lemonades,” Van recalls. They share a laugh and Rha adds, “We learned how to drive in Berkeley Square because the streets, there was no traffic. It was so comfortable then.”

But just months after the Nickersons moved in, rumors began to spread that yet another threat to Sugar Hill was looming — a freeway. It was part of a federal push in the 1950s to modernize America’s roadways, and many of these highways ultimately cut through communities of color. The proposed plans called for the Santa Monica Freeway to run east to west, razing Berkeley Square completely and splitting Sugar Hill in two.

“I remember quite vividly and I remember my father being so upset. …I remember meetings with homeowners in Berkeley Square,” Rha Nickerson says. Some of those homeowners banded together and lobbied against the freeway at the state Capitol.

But this time, all they were able to accomplish was delaying the project. The California Highway Commission unanimously approved the freeway that would decimate Rha and Van Nickerson’s childhood home. Van remembers looking outside of his bedroom window. “I watched the tractor bulldoze these homes down.”

The government seized the Nickersons’ home through eminent domain — and while the U.S. Constitution requires “just compensation” for any property acquired this way, residents who lost their homes were not entitled to assistance from the government in finding and moving to new homes.

Rha Nickerson felt her family was cheated. “I remember my father telling me about eminent domain, and how there was no option to stop this. The valuation for our home was quite low; it was not market value that we were compensated for. And so it was quite an upheaval.”

It was an upheaval Rha’s father told her would never have happened if Sugar Hill were a white neighborhood. “He was very, very angry. He felt the city government resented Black people living there, and this is their way of demolishing a very viable community to support racism,” she says.

At the time, highway planners used the language of science to justify building freeways through communities of color, says Eric Avila, a professor of urban studies at UCLA. “They presented a kind of dizzying array of charts and graphs to insist that this was the most economically efficient route for this particular freeway. They denied any questions of race, they denied any questions of bias.”

What they did instead, Avila says, was say they were targeting so-called “blighted” communities. “I don’t think we know the extent to which Sugar Hill was designated a blighted area because it was affluent. … But in the discourse of urban planning in the mid-20th century in the United States, blight was often synonymous with people of color and with African Americans in particular.”

By 1963, the construction through Sugar Hill began and Rha and Van Nickerson’s family home was replaced with traffic lanes. Around that time, the California Division of Highways proposed another freeway that would cut through Beverly Hills. But when that wealthy white community protested, officials canceled construction.

Almost 70 years later, the Nickersons still feel the loss of their childhood home. “It was just sad,” Rha Nickerson says. “I didn’t know what to expect because that’s all I knew was Berkeley Square, and I really felt very secure in the community. So I was quite rattled by it all.” She and her brother say that after the freeway forced them out, they never quite experienced the same safety and comfort that Sugar Hill provided.

Van Nickerson recalls a particular moment when he knew things had changed. “We moved over onto Bronson Avenue and I immediately got into some problems. Most of that neighborhood was white and a white boy called me a n***** in front of my house. And pardon my vernacular, but I kicked his ass. You know, that was the beginning of the real world for us.”

For many of the residents in the area today, deafening road noise, toxic pollutants, and the resulting health conditions they cause are part of everyday life. This pattern has played out in cities all across America — affecting communities of color most.

Before Van and Rha Nickerson parted ways during a recent visit to their old neighborhood, they closed their eyes and listened for the sounds of their beloved Berkeley Square one more time — only for Van to hear “the rumbling of the automobile.”

“That was nonexistent when we were kids. It was quiet,” he said. Rha nodded in agreement, adding, “You can’t hear the birds anymore.” She headed to the corner to catch the next bus to Inglewood, where she lives now.

Van got into his car to begin his journey home to a town more than an hour away. His drive would begin on the Santa Monica Freeway — and take him right through the middle of what was once known as Sugar Hill.

As the construction that made Los Angeles “the city of freeways” ramped up in the early 1960s, white Americans continued to move to newly developed suburbs that dotted the borders of urban city centers.

It had been nearly a decade since racially restrictive covenants had been lifted, so slowly, more neighborhoods were opening up to Black residents like Robert Lee Johnson’s family.

Johnson and his two brothers lived in a public housing complex in South LA until his mother Gaynelle became an X-ray technician and married his stepfather, James Ferguson, who was an aerospace engineer. In 1961, they bought property from a white couple just north of downtown Compton, a suburb just south of downtown Los Angeles.

Johnson remembers moving-in day. “I see moving vans, trucks and everything all down the street,” he says. Johnson was 5 years old at the time, so he says he thought “it was moving day for everybody.” And he noticed that all the other families moving in were were Black, too.

In the years before covenants had been deemed unconstitutional, Compton was a nearly all-white city. Suddenly, when covenants were lifted, the real estate industry recognized a new, untapped market could be targeted for home sales.

But for Black people to move in, existing homeowners would have to make way. So, the real estate industry targeted white homeowners to convince them to sell their homes using a scheme known as blockbusting.

The underlying idea was to create panic among white homebuyers by creating the expectation that Black homebuyers were moving in and would, in turn, lower property values in their neighborhoods. There are accounts of real estate agents recruiting Black people to walk around white neighborhoods with strollers to create the impression that African American families were settling in.

Agents would convince white homeowners that their houses were losing value by the day because of the looming threat of Black neighbors, so the homeowners would panic and sell. Then, the agents would turn around and sell those homes at inflated prices to Black buyers — who were eager to make a start in better neighborhoods.

Kitty Felde, who is white, grew up in Compton in the 1960s and remembers a flyer appearing under her family’s front door. “It had one very clear message and it was, ‘Sell now, because you’re never going to be able to get the money you want for your house.’ And they didn’t say this but it was like, they are moving in.”

Felde says it was clear the flyers were referring to African Americans. In the years to come, she began noticing the neighborhood changing and new faces at school. Her family chose to stay, but many white neighbors fled and families like Robert Johnson’s took their place.

Johnson has warm memories of the years that followed “moving day” in 1961. He says Compton felt like a “step into another world” compared with the public housing complex his family was living in prior to their move. Though their new home was shared with his brothers, it was spacious. He recalls having fruit trees in his backyard — oranges, loquats and persimmons. “I didn’t know what a loquat was until I got to Compton!”

He remembers going to a local recreation center and park to learn how to swim, play basketball and perform in community Christmas plays. “Our parents were involved, you know. Your father was out there being a coach, the mothers were out there supporting the team, selling hot dogs.” He says it was a typical American suburb.

Until the mid-1960s, Compton was a thriving Black city with Black political power — it had elected its first Black councilman, Douglas Dollarhide, who eventually went on to become the city’s first Black mayor. Union jobs were opening up to Black workers, and Compton was home to better, integrated schools and a city college.

But while Compton represented social mobility for many Black Americans, it also came to represent their exploitation. Predatory practices, like blockbusting, forced families to overpay for homes that would eventually decline in value as more Black residents arrived. According to census data, the median home price in Compton in 1960 was $12,800. Johnson’s family paid $17,500 — or 37% more — despite it being a smaller home than most in Compton at the time.

Josh Sides, a professor of history at California State University, Northridge, says those numbers strongly suggest Johnson’s family was a target of blockbusting. And after more Black residents moved in, home prices languished in Compton over the next several generations.

“The really evil part of blockbusting, in my view, is that it perpetuated the notion that Black people in your neighborhood diminished value,” Sides says. “And because of that perception, it became a self-fulfilling prophecy. That is, it became true that a Black person moving to your neighborhood meant your value declined because, of course, property values are largely the function of social decision and social beliefs.”

By 1970, Compton’s Black population had reached 71%. But as more white residents left, their businesses and tax base did, too. A number of economic factors also led to fewer manufacturing jobs in the area, which were the backbone of Compton’s steady employment. Around this time, industrial jobs had largely moved to LA’s suburbs, unemployment in Compton was skyrocketing, and it continued to worsen into the next decade.

Johnson remembers some neighbors began having trouble making their mortgage payments. “The first time I really noticed it personally was at school because you’re sitting in class and your classmates are gone,” he says.

That’s when he recognized something had changed. Wilson Park, where he had had taken swim lessons and played basketball, was suddenly without paid adult supervision, which Johnson remembers resulting from a loss in the city’s revenue.

“People in Compton were put in a very bad position,” he says. “Legitimate jobs were gone, and then comes this — it’s more than a drug. It was almost like a demonic spirit.” He is referring to the crack epidemic that took hold in Compton during the 1980s.

Nearly three decades after his family had purchased his childhood home in Compton, Johnson realized he didn’t want to raise his own son in his beloved city.

“One day, I’m sitting in front of my house washing my car, and some fool from a block away had gotten a new rifle and he starts shooting out the street lights.” To protect his son, Johnson felt he had no option but to leave Compton.

When Johnson’s family sold their home in 1988 for $64,000, it was worth less than what they paid in 1961. Adjusted for inflation, that house lost nearly 8% of its value over 27 years.

But even though Johnson left Compton, Compton never really left him. He’s written a book about the city’s history, he’s a founding member of the city’s historical society, and you can see his face brighten instantly when he spots an old neighbor during a recent visit.

Robert Johnson was just one of thousands of Black Comptonites who began streaming out of the city in the 1980s in search of more space and safer neighborhoods. The face of the once majority Black city was changing quickly as its African American residents largely moved inland to newly built exurbs.

Billy Ross, now 45, spent the 1980s and early ’90s growing up in Compton just as Johnson was relocating his family. “Compton was changing around us — and fast,” Ross says.

He describes his childhood there as both “magical” and “incredibly challenging.” Magical because it was a largely Black city with political power, which meant there was diversity within the Black community. “It was a spectrum of people, a spectrum of Black class … you know, from professional people to people [that] are just getting by. I mean, that’s magical.”

Ross’ eyes crinkle and a smile spreads across his face when he recalls sitting on his front porch as his sister would braid his hair and a neighbor would walk past, making spontaneous plans to play a game of dice around the corner. He says there was always something exciting happening on his block. But then his smile fades. “The Compton I grew up in really doesn’t exist anymore.”

But the “incredibly challenging” part of growing up in Compton, he says, came when the crack epidemic and its ripple effects hit. Economic inequality and police violence against Black people in Los Angeles were at a fever pitch. The rising tension between law enforcement and African Americans erupted in the 1992 uprising when four police officers were acquitted after brutally beating a Black man named Rodney King.

Ross’ relatives and neighbors began trickling out of the city in search of more space, good schools, and safety. It was also becoming increasingly unaffordable to purchase property in Los Angeles County. Like many others, Ross’ relatives turned their gazes to the Inland Empire — a stretch of land that began about 50 miles east of LA. Not long before, it had been mostly desert, vineyards and factories.

But then, a window of opportunity opened for potential Black homebuyers when newly developed cities like Rancho Cucamonga cropped up. Ross remembers visiting his relatives nearby. “None of this existed. … These houses were built like ’06, ’07, ’08.” By the early 2000s, so many from Compton had relocated to the Inland Empire that one of its neighborhoods became known as “Little Compton.”

Ross recalls his impression of life in the Inland Empire as a teenager. “It’s like, ‘You guys are going to buy a five-bedroom house and you’re going to have a pool. Like what? That’s super fly … and people were willing to commute for that.” Even though housing was cheaper and more spacious in the Inland Empire, most jobs stayed in LA, which meant commuters spent anywhere from three to five hours in rush-hour traffic per day.

Ross’ parents chose to stay in Compton. Their philosophy was, “don’t move, improve.” That’s a phrase Ross says Black people hear a lot. “In the places where we are en masse, there is often an incentive to leave, and that’s messed up because you don’t get the generational, the institutional, cultural insulation. You don’t get the transfer of energy. And you end up going from where you are rich in so many ways — maybe not financial — but you’re rich. And you go elsewhere looking to carve out some economic security. But culturally, now you are diluted.”

But even for Ross, who holds such allegiance to Compton, moving inland eventually became the most practical option. In 2000, after he had graduated college, he married his wife, Tamara, who rented a home, and then they briefly owned a condominium 25 miles northeast of Compton. A few years later, when they learned they were expecting their first child, they decided they needed more space and had new considerations, like good school districts.

So, in April 2006, the couple zeroed in on a four-bedroom house with a three-car garage in the city of Fontana in the Inland Empire. The entire lot was almost 8,000 square feet. It would cost $525,000.

Their loan officer offered them terms they could not refuse — something commonly known as a NINJA loan. They would have a minimal down payment — far lower than the standard 20% — and they would need no proof of income or assets. All the officer needed was a credit check, which was no problem for the couple because they had high credit scores. It was so easy, and they had been told they could always refinance if they needed a more affordable payment later down the line.

“There was this kind of feel that this is a secret and it’s being brought to the masses now. That was even part of the pitch. … You remember this feeling like, ‘Oh, yeah, this is like the kind of loan white people use.’ You know, like, ‘Why would you use your own money to buy a house?’ ”

Immediately, Ross threw himself into the pleasures of suburban life. “The newness of it was cool. This was a one-story house and it had space inside and outside. And I could water my own grass like my father did. I had grass!” Ross was transitioning into a real estate career at this time, Tamara was climbing the ranks as a prosecutor, and they were growing their family. Life in Fontana was good.

“And then, by the fall of ’07, all hell broke loose,” Ross says. The global financial crisis struck and suddenly, the oasis that was the Inland Empire was beginning to disappear before his eyes. Nearly 16% of homes in the region went into foreclosure, making it one of the hardest hit places in the country.

Many homeowners in the area sought help from the Fair Housing Council of Riverside County, where Rose Mayes is the executive director. “I had to create a whole new [foreclosure] department” because of the high demand for this kind of help, she says. The phone calls from those seeking help were incessant. “They were experiencing pain,” Mayes says. “They didn’t know what to do. … people who thought they had done the right thing for the right reasons and it didn’t happen that way.”

Many people Mayes remembers helping were buying homes or refinancing for the first time, making them more vulnerable to the predatory, subprime loans that were widespread during this time. And she noticed that Black and Latinx people were most commonly targeted for such loans.

This is a pattern that has now been tracked all over the United States. Several studies have found that Black and Latinx borrowers were charged significantly more for mortgage loans than white borrowers with similar financial situations between 2004 and 2008.

A financial innovation called “mortgage-securitization” incentivized investors to sell as many loans as possible. Lenders would often steer homebuyers who could have qualified for conventional government mortgages into riskier loans that put more money in the lenders’ pockets — telling buyers they could have a bigger house, lower payments, or both.

The people who were disproportionately targeted belonged to the same communities that had been redlined, locked out of neighborhoods because of racially restrictive covenants, and blockbusted. Now, predatory loans would take away the wealth that so many had spent their lifetimes building.

By 2008, Ross says his house was worth half of what he paid for it two years earlier. But his mortgage payments didn’t reflect that decreased value. He and his wife were paying two times what neighbors were paying to rent the homes along his street — many of them homes that had been foreclosed on by banks.

Homeownership did not shape up to be what Ross once thought — a promise to pass on wealth and security to his children.

Ross says he tried to refinance time and time again because what he was paying was becoming unsustainable. But the lenders refused — because ironically, as long as he kept paying his mortgage every month, they had no incentive to cut him a better deal. He thought, ” ‘Oh, I know this game,’ and that was tough because you have made a commitment … and the commitment is tied, in a way, to your identity. You see yourself as a certain type of person.”

But after paying what he says felt like an exorbitant mortgage for several years, “Tamara and I ultimately decided that these people don’t give a damn about us. And they are content to bleed us dry.”

So they stopped paying. Ross knew their credit scores would tank and they would have to swallow that hit for years to come. But he also knew this strategy was the only chance they had to hold on to their house.

Eventually, about two years after they employed a “strategic default,” Billy and Tamara Ross’ gamble worked. A lender finally agreed to help them refinance. They spent years building up their credit score again. In 2019, they were able to sell the house in Fontana and move into a new one nearby.

Mayes, of the Fair Housing Council, says many homeowners in the Inland Empire are still reeling from the financial crisis. Others she remembers helping simply disappeared, she says.

Billy Ross considers himself one of the lucky few Black people who made it out, despite a system he thinks is designed to keep African Americans on the bottom.

“It really makes me sad,” he says. “There ain’t a whole lot of us on this side where we’re able to function and kind of take advantage of some of the things that this society has to offer. A lot of us, we don’t own property. We don’t have equity in the stock market. We don’t have equity in this country. We don’t own stuff. And ownership is equity.”

That is why Ross isn’t wasting his second chance. He and his wife have been building what Ross calls his soon-to-be “forever home.” He recalls a recent conversation with a loan officer who was trying to lock him into a loan now — promising that if he didn’t like the terms, he could “just refinance” down the road.

It was all too familiar to Ross, who thought, ” ‘This guy’s asking me to gamble.’ And I told him … ‘Dude, I’m Black. … We’re going to measure twice and cut once. And we’re probably going to keep this house forever, whether we live in it or not. It’s going to belong to our children.’ ”

For Ross, passing on that property is not just about leaving behind a house for his kids. It’s about passing the baton to the next generation, and the one after that — so that one day, they have something to call their own.

A few months ago, DonnaLee Norrington celebrated her 60th birthday in the newly purchased Compton home she and her sister, MaryJosephine, now call their own. Norrington thought she would never own a home again after losing the condominium she and her ex-husband briefly owned before the financial crisis. She said losing that home had turned her credit upside down and from that point on, she rented.

“I didn’t even consider homeownership just because I thought it was out of my grasp — not so much financially, but just the fact that maybe I was too old to own a home and I just didn’t want all the responsibility that came with it,” Norrington says.

Then, she had that dream in which God told her to go to Mark Alston, the mortgage broker, to buy a home with a fixed mortgage. Alston says he understood Norrington’s vision, but “she started crying before we closed. I told her to wait. Let’s get all the way done before we celebrate.”

Alston says he got into real estate because he wanted to do something for his community — for people like Norrington — to change the persistent gap between Black and white homeownership. “I mean, it’s pretty unbelievable to me [that] almost 75% of the white community owns houses. … And in my community, you know, it’s like 2 out of every 10 in LA, 4 out of every 10 in the country,” he says.

Alston has mostly Black clients in and around LA. He says there are complex, systemic barriers holding Black Americans back from homeownership, many of them tied to the process of acquiring an affordable loan that actually allows them to retain and pass on generational wealth.

In order to simply qualify for a loan, a potential borrower must be favorably “creditworthy” according to the lender. In the existing financial system, it is the FICO credit score that primarily determines that creditworthiness, but a third of Black Americans do not even have one.

And for those who do, Alston says, the scores are not as fair or predictive as they could be because the score does not factor in a wide range of payments ordinary people pay. For example, cellphone bills, utility bills and even rental payments are not included in the FICO scores lenders typically use.

Many financial experts agree that these kinds of payments are good indicators of one’s ability to pay a monthly mortgage. Laurie Goodman of the Urban Institute told NPR, “I would assume that if you are looking at my credit score, whether or not I make rental payments is far more predictive than whether or not I pay my Macy’s credit card — but my Macy’s credit card is included and rental payments are not.”

Alston says, in the case of DonnaLee Norrington and her sister, while they did qualify for decent loans with their existing credit situations, a little bit of guidance in paying off bills and waiting for negative portions of their credit history to expire helped them get a better rate, and eventually, qualify for a refinance. “A lot of people have disputes with credit over a $200 or $300 cable box bill,” which he says could significantly lower credit score.

Not all mortgage brokers help their clients dig through paperwork and small disputes to get a better loan. But Alston says most Americans lack an understanding of a complex financial system, so this kind of guidance goes a long way. “It has nothing to do with intelligence. It has to do with familiarity with financial operations,” he says.

Beyond credit scoring, an additional barrier to homeownership became more prevalent after the financial crisis — risk-based pricing, which essentially means the riskier the borrower, the more a lender charges that borrower to loan them money.

About half of Black homebuyers get loans backed by the mortgage giants Fannie Mae and Freddie Mac, which primarily use a borrower’s credit score and down payment to measure the risk that will determine the cost of the loan. Because the average Black borrower’s credit score is about 60 points lower than the average white borrower’s score, and because Black buyers, on average, make smaller down payments, risk-based pricing tends to drive up costs for the average Black homebuyer.

Prior to the global financial crisis, Fannie and Freddie used risk-based pricing to a limited degree, but they generally enabled a broad spectrum of borrowers to access fairly similar rates on their loans. But in response to the crisis, the mortgage giants got more aggressive with risk-based pricing — which disparately affects borrowers with less wealth and lower credit scores. Alston calls this “the poor-pay-more fee.”

Economist Ed Golding worked at Freddie Mac during the crisis. Now at the Massachusetts Institute of Technology, he has analyzed how these extra charges affect Black homeowners’ wealth. “It’s inherently unfair that basically we raised the prices during the financial crisis so that these people who were hurt by the financial crisis could bail out the financial institutions,” he says.

Golding says homebuyers with less wealth and lower credit scores are still being asked to pay more today. “It seems that we’re asking the victims to pay and to pay again for what was really not their fault,” he says.

In separate statements to NPR, Fannie Mae and Freddie Mac said this type of pricing helps them manage risk, and has “provided stability during the pandemic and enabled homeownership for millions of families, including many families of color.”

A third barrier to homeownership that disproportionately affects Black borrowers is mortgage insurance, which is typically required if a borrower makes a down payment that is less than 20% of the loan amount. In fact, 9 in 10 Black homebuyers pay for mortgage insurance compared to only 6 in 10 white homebuyers. And insurance is just another way the financial system accounts for risk — the cost of which is passed on to the “risky” homebuyer.

The Fair Housing Act does not consider any of these risk-based barriers to be illegal. Until now, courts have ruled that lenders can price loans in ways that disproportionately disadvantage certain racial groups if that pricing is related to credit risk. But researchers at UC Berkeley have been exploring a fourth barrier that has nothing to do with credit risk: outright discrimination.

The researchers analyzed nearly 10 million home loans and found that Black and Latinx borrowers are still being charged more, even after controlling for risk. That means Black and Latinx homebuyers with the same credit score and percent down payment as white homebuyers are still paying more for their loans, despite posing no additional risk to the lender — which amounts to illegal discrimination, based on past court rulings.

The study also found that the higher the concentration of Black or Latinx residents in a neighborhood, the more Black or brown buyers in that neighborhood are overcharged.

“This effect is much more pronounced when we cut by geography,” says Robert Bartlett of Berkeley Law, one of the authors of the study. “And so, it is a legitimate concern that basically, this is kind of the new redlining that we’re faced with.”

In this case, rather than refusing to insure loans in Black and brown neighborhoods, lenders simply appear to be charging marginally higher rates to people who live in those neighborhoods. And the effect holds true even when computer algorithms are writing the loans. Their findings will appear in a forthcoming issue of the Journal of Financial Economics.

This idea, of including Black Americans in the housing market but charging them more to do so, is part of what Princeton scholar Keeanga-Yamahtta Taylor calls “predatory inclusion.”

“Once you pay this fee, that fee, this higher amount of money, now you get to participate equally with your white peers,” Taylor says. “And so not only does that impact the way that housing is supposed to generate wealth for people — it cuts into the wealth, the amount of money African Americans have to pay to enter into the housing market in the first place.”

The cumulative effects of these legal policies and discriminatory practices mean Black Americans pay more to own a home — what some experts call a “Black tax” on homeownership. It also means they accumulate less wealth over their lifetimes than white Americans — on the order of tens of thousands of dollars of lost savings and investments, according to an analysis by MIT’s Golding and his colleagues.

And while lenders and mortgage companies may say risk-based pricing is a fair way to account for risk, the broker Mark Alston has a different view of what “fair” means in America. “When you’ve had 350 years of not just unfairness but actual opposition — you had exclusionary zoning laws, you had private covenants, you had federally institutionalized redlining, now you have disparate housing finance policy. When you have actual opposition, ‘fair’ is an interesting concept.”

Alston says “a good head start beats fast running,” and worries that a 350-year head start for white Americans could mean Black Americans may never catch up — unless the financial system is changed to be more affirmatively equitable.

“I could care less about Black Lives Matter being painted on [a] basketball court,” he says. “How about an affirmative program to lower the gap between white and black homeownership? How about actual public policy that moves the needle, for real? How about a change in employment and pay that narrows the gap, the inequities between white and black pay? How about those type of things that will make a difference for future generations?”

In a statement to NPR, the National Association of Realtors, the largest real estate group in the country, acknowledged its past role in housing discrimination and said it has implemented anti-bias training programs for its members.

“Decades of systemic racism have left millions of minority households behind, a system NAR regrettably helped perpetuate a half century ago,” the group said. “Over recent years, NAR has recommitted itself to rectifying mistakes of the past, dismantling lingering nationwide housing inequities, and advocating for policies which ensure the market is more accessible in the years to come.”

Among his first executive orders, President Biden in January directed the Department of Housing and Urban Development “to take steps necessary to redress racially discriminatory federal housing policies.”

Alston plans to continue pushing for policy change that increases access to Black homeownership, all the while enhancing access through his own practice for people like DonnaLee Norrington.

Back on her quiet tree-lined street in Compton, Norrington sheds tears through a big smile as she reflects on her accomplishment. “I always feel like a late bloomer,” she says, but owning her own home is a relief.

“We don’t ever have to worry about, you know, somebody gonna sell it from up under us or anything like that,” she says. “We got our own little piece here. … I feel really good about that, you know, leaving some sort of legacy.”

It’s a legacy that remains out of reach for many Black Americans today.

CREDITS: Ailsa Chang/Christopher Intagliata/Jonaki Mehta/NPR